In performing an attestation engagement a cpa typically – In performing an attestation engagement, a CPA typically takes center stage, assuming specific responsibilities and adhering to established standards to provide assurance on subject matter.

This comprehensive guide delves into the intricacies of attestation engagements, exploring the CPA’s role, applicable standards, and the procedures involved in conducting such engagements.

1. Purpose and Scope of Attestation Engagements

Attestation engagements are professional services performed by CPAs to provide assurance on the reliability of information.

The primary purpose of an attestation engagement is to enhance the credibility of information by expressing an opinion or conclusion about the subject matter.

Attestation engagements encompass a wide range of services, including audits, reviews, and agreed-upon procedures.

The scope of an attestation engagement is defined by the agreed-upon procedures between the CPA and the client.

Limitations of attestation engagements include the inherent uncertainty of the subject matter, the use of sampling techniques, and the reliance on representations made by management.

2. CPA’s Responsibilities

CPAs have specific responsibilities in performing attestation engagements, including:

- Exercising due professional care in planning, performing, and reporting on the engagement.

- Maintaining independence and objectivity throughout the engagement.

- Obtaining sufficient and appropriate evidence to support their opinion or conclusion.

- Reporting on the results of the engagement in accordance with applicable standards.

Due professional care requires CPAs to act with the skill, care, and diligence expected of a reasonably prudent professional.

Independence and objectivity are essential to ensure that the CPA’s opinion or conclusion is unbiased and reliable.

3. Attestation Standards

Attestation engagements are guided by a set of standards established by the American Institute of Certified Public Accountants (AICPA).

The primary standard for attestation engagements is Statement on Standards for Attestation Engagements (SSAE) No. 18.

SSAE No. 18 establishes five key principles that must be followed in performing attestation engagements:

- Independence

- Due professional care

- Sufficient evidence

- Reporting on findings

- Quality control

These principles provide a framework for CPAs to ensure that attestation engagements are performed with the highest level of professionalism and objectivity.

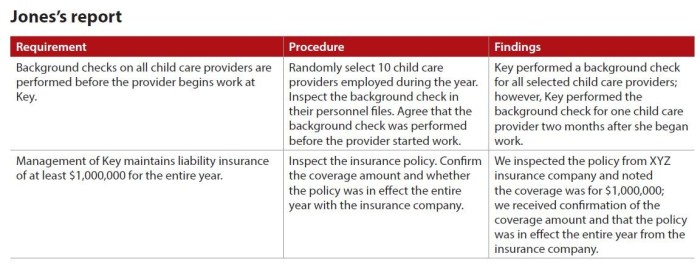

4. Attestation Procedures: In Performing An Attestation Engagement A Cpa Typically

CPAs perform a variety of procedures during an attestation engagement, including:

- Analytical procedures

- Inquiry and observation

- Inspection and examination

- Confirmation

Analytical procedures involve analyzing financial and non-financial data to identify unusual trends or relationships.

Inquiry and observation involve gathering information through interviews with management and observation of processes.

Inspection and examination involve reviewing documents, records, and physical assets.

Confirmation involves obtaining written responses from third parties to verify the accuracy of information.

| Analytical Procedures | Inquiry and Observation | Inspection and Examination | Confirmation |

|---|---|---|---|

| Compare financial ratios to industry averages | Interview management about internal controls | Review bank statements | Confirm accounts receivable with customers |

| Analyze trends in sales and expenses | Observe inventory counting procedures | Inspect equipment for proper maintenance | Confirm liabilities with creditors |

General Inquiries

What is the primary purpose of an attestation engagement?

The primary purpose of an attestation engagement is to provide assurance on the reliability of subject matter, typically financial or non-financial information.

What are the different types of attestation engagements?

The three main types of attestation engagements are examinations, reviews, and agreed-upon procedures.

What are the key principles of SSAE No. 18?

The key principles of SSAE No. 18 include independence, due professional care, sufficient and appropriate evidence, and reporting on findings.